unified estate tax credit 2020

It mainly serves the purpose of preventing taxpayers from giving away too much during their lifetimes in order to avoid estate taxes. Estate tax exemption which may also be expressed in the form of a unified credit.

Irs Announces 2017 Estate And Gift Tax Limits The 11 Million Tax Break

For example lets say you give away 506 million in assets during your lifetime.

. For more information see the General Information section and the instructions for lines 13 and 26 on Form ET-706-I and also TSB-M-19-1E. Non-resident aliens are entitled to a US estate tax unified credit of 13000 which exempts 60000 of property from estate tax. It can be used by taxpayers before or after death integrates both the gift and estate taxes into one tax system is adjusted for inflation and has no income limit.

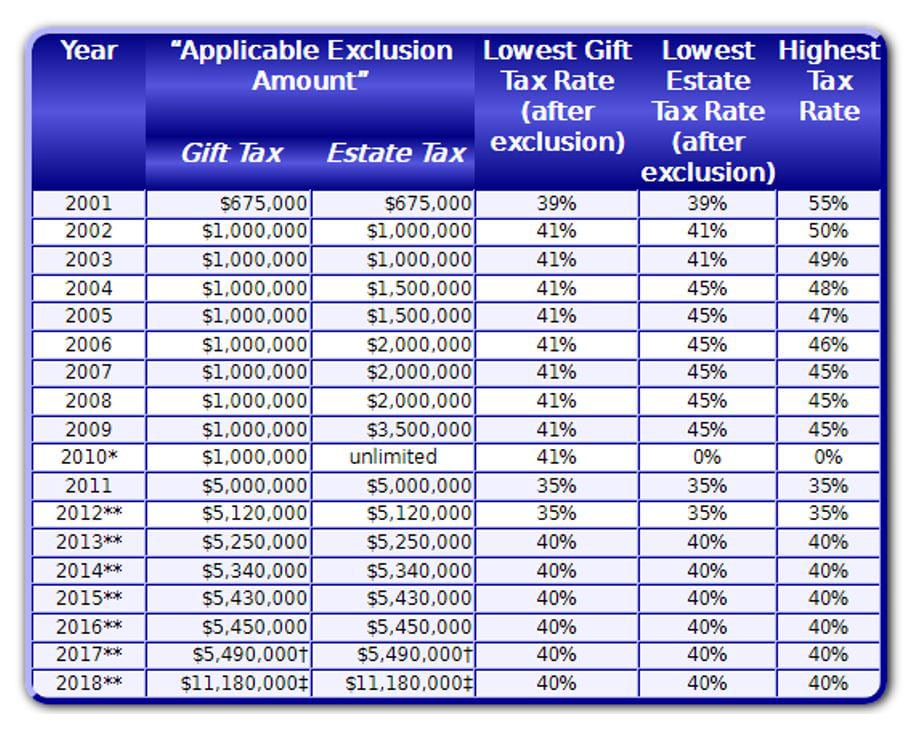

In 2010 the estate tax will be repealed and then reinstated in. That number is used to calculate the size of the credit against estate tax. It just keeps getting better for wealthy individuals.

This means that the federal tax law applies the estate tax to any amount above 1158 million for individuals and 2316 million for married couples. Gift Tax 5490000 11180000 11400000 11580000 Estate Tax 5490000 11180000 11400000 11580000 Applicable Credit Amount. In addition to the unified tax credit individuals can give up to 15000 a year to a recipient or recipients 15000 per gift to as many recipients regardless of how many people you gift and not have to pay a gift tax.

Learn How EY Can Help. Estate Planning 2017 2018 2019 2020 Annual Gift Tax Exclusion 14000 15000 15000 15000 Annual Gift Tax Exclusion to a Noncitizen Spouse 149000 152000 155000 157000 Applicable Exclusion Amount. Situs property transferred to your heirs Please contact us.

The tax is then reduced by the available unified credit. The unified tax credit is designed to decrease the tax bill of the individual or estate. The previous limit for 2020 was 1158 million.

Ad Committed to Delivering High-Quality Tax Services for Sophisticated Financial Needs. The estate tax is a complicated and nuanced topic. The amount of property the federal government allows a person to transfer during life or after death without paying gift or estate taxes together called transfer taxes.

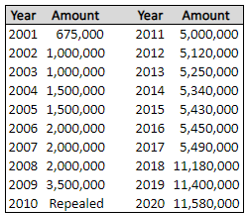

The basic exclusion amount for determining the unified credit against the estate tax will be 11580000 for decedents dying in calendar year 2020 up from 11400000 in 2019. In other words use it or lose it. For gifts made and estates of decedents dying in 2020 the exclusion amount will be 11580000 per person up from 11400000 in 2019.

For 2020 the basic exclusion amount will go up 180000 from 2019 levels to a new total of 1158 million. The 117 million exception in 2021 is set to expire in 2025. The basic exclusion amount for determining the unified credit against the estate tax will be 11580000 for decedents dying in calendar year 2020 up from 11400000 in 2019.

The annual gift tax exclusion amount remains at 15000 but the gift tax annual exclusion for gifts of a present interest to a spouse who is not a US. Estate Trust Tax Services. Forbes put together a great summary with additional tax tables and information about the 2020 standard deduction capital gains rates and other inflation-adjusted items.

Any tax due is determined after applying a credit based on an applicable exclusion amount. The applicable credit amount is commonly referred to as the Unified Credit because it is both unified ie it is a single amount that is applied to transfers otherwise subject to either the gift tax or the estate tax and a tax credit ie it reduces the amount of tax owed. The unified tax credit gives a set dollar amount that an individual can gift during their lifetime and pass on to heirs before any gift or.

The cap amount is 1206 million in 2022 up from 117 million in 2021. A key component of this exclusion is the basic exclusion amount BEA. For 2020 US residents and citizens are entitled to a US estate tax unified credit of approximately 4577800 which essentially exempts 1158 million of property from estate tax.

How Might the Biden Administration Affect the Unified Tax Credit. The Tax Law requires a New York Qualified Terminable Interest Property QTIP election be made directly on a New York estate tax return for decedents dying on or after April 1 2019. That exemption amount is 2 million in 2008 and will go up to 35 million in 2009.

The estate and gift tax exemption is. In general the Gift Tax and Estate Tax provisions apply a unified rate schedule to a persons cumulative taxable gifts and taxable estate to arrive at a net tentative tax. Youd have just 7 million left of that 1206 million credit with which to.

For 2021 the estate and gift tax exemption stands at 117 million per person. The lifetime gift tax exclusion in 2020 is 1158 million meaning the federal tax law applies the estate tax to any amount above. The amount of the Unified Credit is currently higher than it has ever been while an estate tax is.

Minimize Taxes Through Estate Planning. You can also read more about higher retirement plan contribution limits for IRAs 401ks and more. For example for 2020 the US.

The IRS announced new estate and gift tax limits for 2021 during the fall of 2020. The unified credit is a credit for the portion of estate tax due on taxable estates mandated by the Internal Service Revenue IRS to combine both the federal gift tax and estate tax into one. Most relatively simple estates cash publicly traded securities small amounts of other easily valued assets and no special deductions or elections or jointly held property do not require the filing of an estate tax return.

Qualified Small Business Property or Farm Property Deduction. In 2020 after adjustment for inflation it was raised to 1158 million for individuals and 2316 million for a married couple. Since 2000 the estate and gift tax collectively called the transfer tax has gone from an exemption of 675000 and a top marginal rate of 55 to a n.

Estate tax exemption amount is US1158 million which if expressed as a unified credit amounts to US4577800. The Internal Revenue Service recently announced the inflation-adjusted estate and gift tax exclusion amount for 2020. To claim a portion of a US.

Estate tax returns are required when the total gross value of the estate exceeds the amount shown in the following table. The Internal Revenue Service announced today the official estate and gift tax limits for 2020. The exclusion amount in 2021 increased to 11700000.

A Look At 2020 Cost Of Living Adjustments And Estate Gift Tax Limits Cpa Boston Woburn Dgc

Historical Estate Tax Exemption Amounts And Tax Rates 2022

How Do State Estate And Inheritance Taxes Work Tax Policy Center

Exploring The Estate Tax Part 2 Journal Of Accountancy

/UnifiedTaxCredit-d90e228472aa44e88eebc9866e3045d9.jpg)

Unified Tax Credit Definition

Historical Estate Tax Exemption Amounts And Tax Rates 2022

2021 Cost Of Living Adjustments And Estate Gift Tax Limits Cpa Boston Woburn Dgc

History Of The Unified Tax Credit Apple Growth Partners

What Is Estate Tax Quora

Estate Tax Primer For German Investors In U S Real Estate Partnerships Dallas Business Income Tax Services

Estate Tax Primer For German Investors In U S Real Estate Partnerships Dallas Business Income Tax Services

What Is The Unified Tax Credit How Does It Change Federal Gift And Estate Taxes

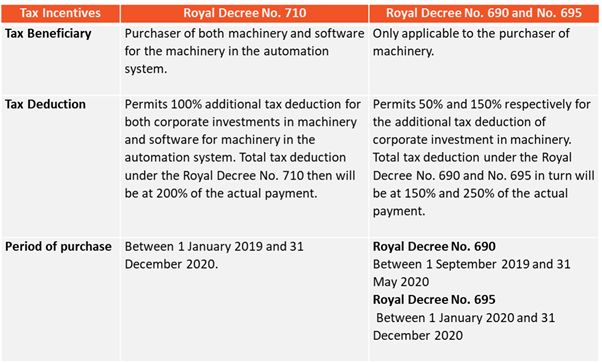

200 Tax Deduction In Thailand For Investment In Automation System Tax Thailand

How The Unified Tax Credit Maximizes Wealth Transfer Blog Jenkins Fenstermaker Pllc

:max_bytes(150000):strip_icc():saturation(0.2):brightness(10):contrast(5)/WhatIsaUnifiedTaxCreditAug.92021-f598bf82c87b42a7b139f10953ad3850.jpg)

What Is A Unified Tax Credit

How To Advise Your Clients Under The New Estate Tax Law Ppt Download

U S Estate Tax For Canadians Manulife Investment Management

Gift Tax Unified Tax Credit Estate Tax Corporate Income Tax Course Cpa Exam Far Youtube

Tax Related Estate Planning Lee Kiefer Park